During the last meeting held at the end of July, the Bank of Japan (BOJ) resolved to increase flexibility in the yields of 10-year government bonds. The peculiarity of this situation lies not so much in the decision itself, but in the importance that many experts in the sector have attributed to it.

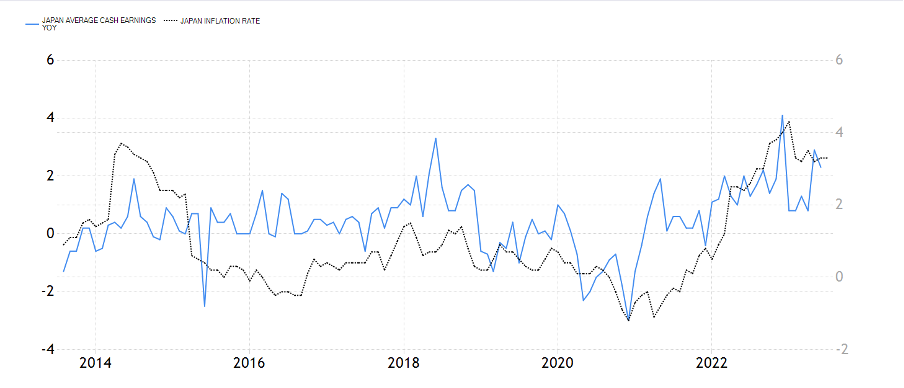

The BOJ opted for further flexibility in 10-year bond yields, moving from a range of 0-0.5% to a new range of 0.5%-1%. This decision, albeit very late, is due to inflation well above the desired targets. What is surprising is that many analysts have given greater emphasis to this move compared to the decisions taken by institutions such as the Federal Reserve or the European Central Bank, which in the same week increased interest rates by 25 basis points, bringing them to 5, respectively. 50% and 4.25%. Currently, Japanese interest rate for short-term maturities is as low as -0.10%.

Many voices emphasized: “The BOJ is getting restrictive! Now the Japanese will sell 10-year US government bonds (which yield 4%) to buy Japanese government bonds (which yield just 0.55%)." This case demonstrates how a superficial reading of the news can distort reality. Emphasize the importance of not just focusing on the present moment, but considering the underlying infrastructure.

The reality is that currently, Japan offers markedly negative real returns, both for maturities both short-term and long-term (among the worst in the world, around -2.5%), while in the United States, real yields vary from 1.5% to 2.5%, depending on the maturities.

Instead of focusing only on the BOJ’s decision, Japan should worry about the medium-term effects on their government bond position. If the central bank were to tolerate yields close to 1%, 10-year bonds could suffer a potential loss of 5%. Until recently, they were protected by central bank purchases, which prevented their devaluation. This protection has now disappeared.

It is ironic how some news can easily be distorted by industry experts, the same ones who at the beginning of the year suggested preferring the bond market to the stock market.

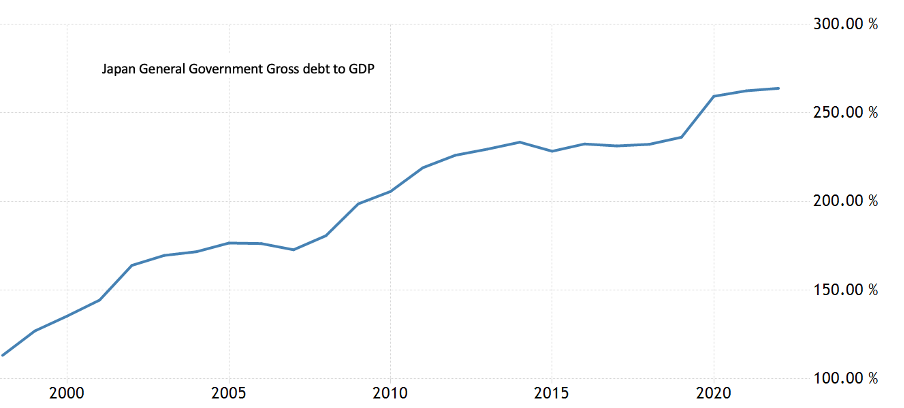

It is a fact that the BOJ has few options for dealing with inflation. On the contrary, if inflation were to rise significantly, it could become the only way to devalue a public debt that has exceeded 250% of GDP, with 60% held by the central bank itself. It should be noted that this debt has grown by more than 150% in about 10 years and not due to the pandemic, but rather crazy structural spending in order to maintain a growth rate above zero and not fall into deflation.

Original article published on Money.it Italy- 2023-08-29 07:54:28. Original title: Giappone, perché la maggiore flessibilità nei rendimenti dei titoli di stato è inutile?-